Show Your Working

Why investors mistake confidence for competence.

I walked out of a parent-teacher interview this evening and I haven’t been able to stop thinking about it.

My son is doing brilliantly in maths. His teacher, who taught him two years ago and has him again now, was genuinely delighted by his progress. More confident. More engaged. Quicker to put his hand up.

But then she paused. She said: he’s very often correct. But he rushes. He gets to the right answer and moves on without showing how he got there.

He’s proud of getting to the answer. The working behind it doesn’t interest him as much.

I sat in that chair and smiled. And then my mind drifted to my daughter, who started high school this year.

She approaches maths differently. She agonises. She reads the question, then reads it again. She works through every step of the logic, slowly and carefully. She doesn’t always get it right. But what she’s most proud of isn’t the result. It’s the steps. The process. Being able to trace back through her own thinking and say: here’s how I got here.

My son is proud of his answers. My daughter is proud of her progress.

Two children. Same gene pool. Almost opposite beliefs about what counts as proof.

I’m not drawing conclusions about either of them. They’re kids and they’re still forming. These orientations aren’t fixed, and they’re not inevitable. They’re being shaped. By what gets praised. By what gets noticed. By ten thousand small signals, in classrooms and at kitchen tables, that tell children what kind of knowing matters.

I sat in that car park for a few minutes before driving home, because I couldn’t shake the thought:

We are already building the conditions for the confidence gap. And we fund the gap like it’s a feature, not a bug.

The Study That Should Haunt Every Investor

In 1999, David Dunning and Justin Kruger ran a study at Cornell. They gave undergraduate students tests on logic, grammar, and humour. Then they asked each student to estimate how they’d done relative to everyone else.

The worst-performing students, in the bottom quartile, estimated they’d scored in the top half. They had no idea how little they knew. The best performers, meanwhile, consistently underestimated themselves. The material felt manageable to them, so they assumed it felt manageable to everyone.

Incompetence, it turns out, is self-concealing. You need a certain level of skill just to recognise how much you’re missing.

I’ve thought about that study since I started paying attention to who gets funded.

The Number That Should Bother Every Investor

Research published in the Journal of Business Venturing found that overconfident entrepreneurs, those who systematically overstated their venture’s prospects, attracted significantly more investor interest and higher pre-money valuations than founders whose projections were grounded and evidence-based.

Yes, you read that right.

The founders who were wrong—confidently, dramatically wrong—were more fundable than the founders who were right.

Investors interpreted inflated projections as ambition and vision. Accurate projections, with caveats and contingencies built in, read as hesitancy. As a lack of belief in the company’s potential.

This is not a quirk at the margins. This is structural bias baked into how funding decisions get made. And once you understand who benefits from it, and who doesn’t, the rest of the gender funding gap starts to make a lot more sense.

Who Benefits From The Gap

It pains me to write this, but research on gender and self-assessment is consistent: women report significantly more pessimistic beliefs about their own performance than men. Even when actual results show no difference. A 2024 Caltech study confirmed it directly: “On every single one of the self-assessment questions, women report more pessimistic beliefs about their performance than men.”

The researchers then tested whether evaluators, once told about the confidence gap, would correct for it. As you might expect, they wouldn’t. Even when explicitly flagged, evaluators continued to rate women as lower performers based on their self-assessments. Awareness, on its own, isn’t enough. The bias holds even when people know it’s there.

As we covered in The Behaviour Penalty, there is no winning formula here. Perform confidence and you’re aggressive. Don’t perform it and you’re unambitious.

In most professional environments, overconfidence gets corrected over time. You hire someone who oversells their capability, they underdeliver, and the feedback loop adjusts.

Early-stage investing doesn’t work that way. The timelines are long. The information is asymmetric. By the time a company’s market assumptions prove false, three more rounds have closed and the original investor has often moved on to the next deal. The feedback loop that corrects for overconfidence in other contexts barely exists here, which means the bias doesn’t self-correct. It compounds.

In this environment, confidence becomes a proxy for quality. Not because investors are foolish. Because they’re human, working with incomplete information under time pressure. Confidence feels like a signal. It registers as evidence.

For founders socialised to project certainty regardless of what they actually know: that's currency. For founders socialised to be accurate, to hedge, to acknowledge what they don't yet know: it reads as weakness.

My son knows the answer. My daughter knows why the answer is correct and, crucially, why a wrong one was wrong.

The room funds my son.

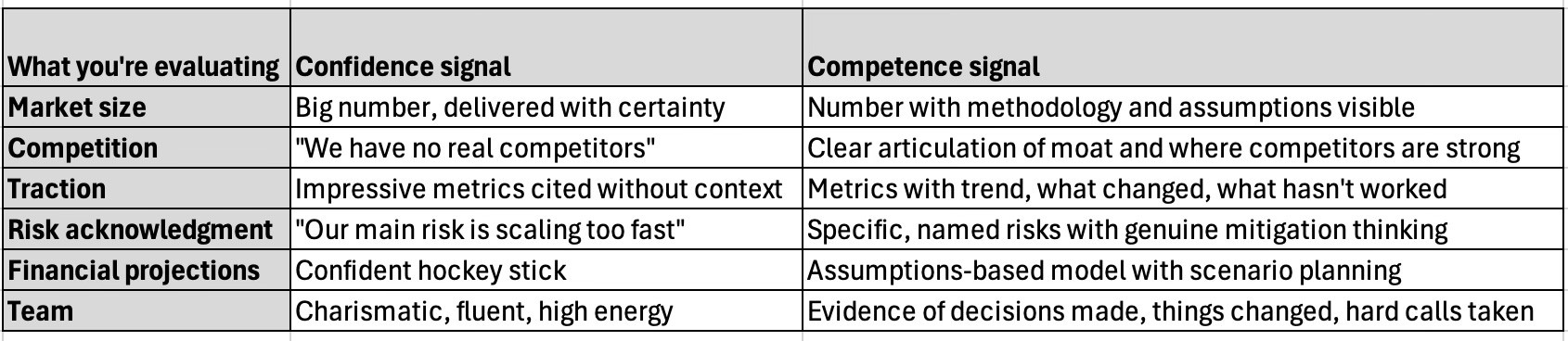

What The Room Actually Rewards

Think about what confidence looks like in the room. It’s a big number said without flinching. Hard questions answered without qualification. Projections delivered with certainty, a market framed as inevitability, a timeline that assumes everything goes right.

Now think about what accuracy looks like. It’s a TAM with the assumptions shown. It’s “we expect 18 months, though we’re stress-testing at 24.” It’s “our main competitor has distribution we’ll need to build.”

All of which is more useful information. All of which is more likely to lead to a successful investment. All of which reads, in that same room, as doubt.

We have built a system that filters for people who are comfortable overstating their certainty. Then we act surprised when those people make decisions that don’t pan out.

Dunning-Kruger, Applied To Capital Allocation

Back to Dunning and Kruger, because their finding has a second edge that matters here.

The best performers in their study consistently underestimated themselves. Not because they were insecure. Because they had enough skill to know what they didn’t know. They could see the complexity that the poor performers couldn’t even perceive.

The founders who’ve done the least work can pitch with the most apparent certainty. They don’t know what they don’t know. That unknowing presents as boldness.

And it gets funded.

I’ve sat on judging panels where I’ve watched this happen in real time. A founder who gave a careful, precise, evidence-heavy pitch; with clear methodology, real customer data, and honest acknowledgment of what they still needed to prove; scored lower on “investor confidence” than the founder who followed them with a big number and a smooth answer to every question.

The careful founder knew more. The smooth founder knew how to perform certainty. The room funded the performance.

What Happens After Failure

When a male founder’s company doesn’t work out, the narrative is generous. He was “too early for the market.” He “took a bold swing.” He learned what he needed to know for the next one.

A 2025 NBER study found that female entrepreneurs who start again after a failed startup raise 53% less funding than their male co-founders from the same failed enterprise. Women are 22% less likely to attract venture capital compared to male co-founders who experienced the exact same failure. Among those who do raise, they secure an average of $31 million less over five years.

The failure was identical. The interpretation of that failure was not.

Not one bad actor in one bad room. A consistent pattern, applied across thousands of decisions, where the same event means something different depending on who it happened to.

And the problem doesn’t stop at perception. The legal infrastructure around startup failure compounds every cultural bias already stacked against founders who’ve tried, learned, and are ready to go again. The rules weren’t designed with iteration in mind. They were designed with punishment in mind.

Failure is not an end. It’s data. It’s the thing that makes the next attempt better. The narrative around it needs to shift: in how investors interpret it, in how the media covers it, and in the rules that govern what founders are allowed to do next.

The competence is demonstrable. The second chance still doesn’t come.

What Competence Actually Looks Like

Confidence is a performance. It can be trained, coached, and optimised for a room. It tells you something about a founder’s ability to recruit, to sell, and to hold a team together through uncertainty — which matters. But it doesn’t tell you whether the market assessment is sound. Whether the unit economics work. Whether the team has the adaptability to navigate what’s coming.

Here’s a quick framework for your next evaluation:

For every signal you registered, ask yourself: was that the founder showing you something real or just performing for the room?

The Cost Of Getting This Wrong

The numbers bear repeating in this context. Two percent. That’s the share of capital that went to all-female founding teams in Australia in 2025. Down from four the year before.

The system is not funding the best bet. It is funding the most confident performance of the best bet. McKinsey’s 2023 analysis of 1,265 companies found gender-diverse leadership teams have a 39% greater chance of financial outperformance. We know this. The room still funds the performance.

If you missed last week’s piece on where the capital actually goes, The Homophily Trap has the full breakdown.

The Change That Is Already Happening

Changing this doesn’t require a values overhaul. It requires process change — at every level.

I was at the Equity Clear Show Us the Data forum this week. It is Australia’s first common diversity data standard for investors. A framework that puts accountability where it belongs: not on how women pitch, but on how investment decisions are recorded, reported, and compared across the ecosystem. More than 80 venture funds and family offices across Australia and New Zealand have already signed on.

The premise is almost embarrassingly simple: we can’t change what we don’t measure.

For years, the sector has been flying blind, because no one was required to collect the data consistently. Equity Clear is changing that. The gaps become visible. The patterns become undeniable. The excuses run out.

At the individual level: use the matrix above. Separate your notes from your impressions after every evaluation — write down what the founder showed you, then write down how the pitch felt, then compare. If they don’t line up, sit with that.

Report what you fund. If you invest in Australian startups and haven’t looked at Equity Clear, that’s where to start. And ask yourself: am I funding what I saw, or what I felt?

Confidence is designed to be felt. Competence is designed to be seen. The tools to tell the difference now exist. The question is whether we use them.

What I’m Carrying Home

My son is going to be fine. He’s bright and curious and I’m proud of him.

But what lit me up tonight was thinking about my daughter. Painstaking. Thorough. Not always right, but always able to tell you where she went wrong, what she tried, what she’d do differently. Proud not of the answer, but of the process that got her there.

That's not a lack of confidence. It’s intellectual honesty. Which is exactly what you want in someone making high-stakes decisions under pressure: someone who can trace their own reasoning, catch their own errors, and update when the evidence shifts.

It’s also exactly what gets marked down the moment she walks into a room that mistakes a smooth answer for a good one.

I’m not going to tell her to perform certainty she doesn’t feel. I’m going to build the room that knows what to do with her.

To the founders who’ve been told your careful thinking is a liability: it isn’t. The system has the wrong filter. We’re working on it.

Vested Angels is an angel syndicate for women ready to move from reading about the gap, to doing something about it. If that’s you, I’d love to hear from you.

Disclaimer: This article is for educational purposes only and does not constitute financial, legal, or investment advice. Always seek qualified professional advice before making investment decisions.

Citations

Kruger, J. & Dunning, D. 1999, Unskilled and Unaware of It: How Difficulties in Recognizing One’s Own Incompetence Lead to Inflated Self-Assessments, Journal of Personality and Social Psychology, 77(6), pp. 1121–1134.

Hayward, M.L.A. et al. 2010, Beyond Hubris: How Highly Confident Entrepreneurs Rebound to Venture Again, Journal of Business Venturing, 25(6), pp. 569–578.

Dannenberg, A. et al. 2024, The Confidence Gender Gap Is Contagious, California Institute of Technology. Reported in Gaskell, A., Research Explores The Gender Confidence Gap, adigaskell.org, 5 August 2024.

NBER 2025, female entrepreneur failure and second-chance funding gap. Reported in Investopedia, Study Shows Female Entrepreneurs Penalized for Failure, 2025.

Cut Through Venture & Folklore Ventures 2026, State of Australian Startup Funding 2025, australianstartupfunding.com. Published February 2026.

McKinsey & Company 2023, Diversity Matters Even More: The Case for Holistic Impact,analysis of 1,265 companies across 23 countries.

Equity Clear / Alberts 2025–2026, Show Us the Data: Building Australia’s First Investor Diversity Data Standard, equityclear.com.au.

This is the most honest piece I've read on the confidence trap in a long time. I see it in every pitch room. The founder who hedges because she actually understands the risk gets marked down for lacking conviction. The one who has no idea what he doesn't know walks out with a term sheet. You've named the mechanism precisely. The room funds the performance. Sharing this widely.

Fantastic articulation of the atrocious funding gap.

Although I am not entirely convinced that “in most professional environments overconfidence gets corrected over time”

In a fascinating, yet galling study, by Cameron Anderson at Berkeley, it showed overconfidence was rewarded — over long term— by higher social status.

Essentially- they found confidence and competence weren’t just indistinguishable, but the former was preferred. The confident rose to the top and stayed there. And who benefited most? The least competent.

Profoundly disturbing…🤔